For anyone moving to Etobicoke, property tax is one of the most significant and least understood recurring costs of homeownership in this district. Unlike mortgage payments, which are fixed and predictable from the moment you sign, property tax involves a layered system of assessment values, municipal rates, education levies, and annual increases that can be difficult to navigate without a clear guide. Whether you are purchasing your first home in Etobicoke, relocating from another province, or comparing the true carrying costs of Etobicoke against Mississauga before making a final decision, this guide provides the most complete and current analysis of how Etobicoke property tax works in 2026 — from how your assessment value is determined to exactly how and when to pay your bill.

How Etobicoke Property Tax Works: The Essential Framework

Since Etobicoke was amalgamated into the City of Toronto in 1998, property taxes for all Etobicoke homeowners have been administered by the City of Toronto rather than a separate municipal government. This means Etobicoke residents pay Toronto property tax rates — not a separate Etobicoke rate — and their bills are issued, calculated, and collected through Toronto’s centralized property tax system.

The Etobicoke property tax bill is composed of three distinct components:

Municipal levy — the City of Toronto’s portion, which funds city services including transit, parks, roads, emergency services, and community programs. This is the largest single component of the total bill and the one most directly affected by City of Toronto budget decisions each year.

Education levy — the provincial education component collected by the City of Toronto on behalf of the Province of Ontario. This portion funds the public school system and is set by the province rather than the city. Homeowners with children in separate Catholic schools pay the same education levy — the allocation between public and Catholic boards is handled administratively rather than through different tax rates.

City building fund — a dedicated levy introduced by the City of Toronto specifically to fund transit and housing infrastructure investment. This component appears as a separate line item on Toronto tax bills and represents the city’s commitment to long-term capital investment funded through property taxation.

Understanding these three components helps homeowners interpret their annual tax bill and understand which level of government controls which portion of what they pay. For newcomers to the city comparing the cost of living in Etobicoke in 2026 against other GTA communities, the total bill rather than any single component is the relevant figure for budgeting purposes.

Toronto Residential Tax Rate in 2026: What Etobicoke Homeowners Actually Pay

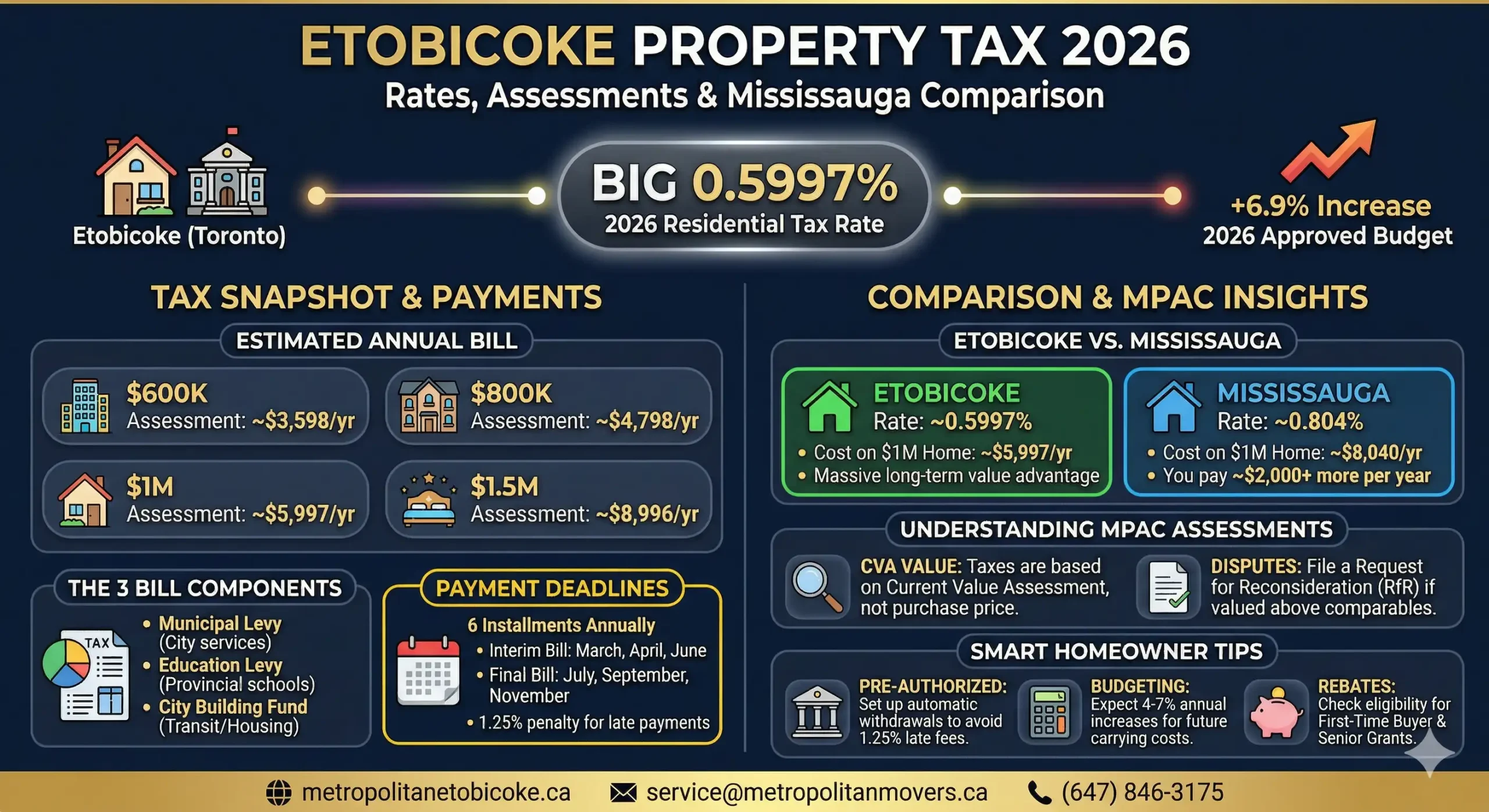

The City of Toronto sets its residential property tax rate annually through the budget approval process. For 2026, the City of Toronto approved a residential property tax rate increase of 6.9% — the combined result of a base rate increase plus the dedicated City Building Levy contribution.

The total residential tax rate for Toronto — and therefore for Etobicoke — in 2026 is approximately 0.599704% of the current value assessment for residential properties. This rate applies to the assessed value of your property as determined by the Municipal Property Assessment Corporation (MPAC), not the market value or the price you paid.

To calculate your estimated annual Etobicoke property tax bill:

Annual Tax = Assessed Value × Total Tax Rate

For a property with a current value assessment of $900,000:

- $900,000 × 0.599704% = approximately $5,397 per year or $450 per month

For a property assessed at $1,200,000:

- $1,200,000 × 0.599704% = approximately $7,196 per year or $600 per month

For a property assessed at $1,500,000:

- $1,500,000 × 0.599704% = approximately $8,996 per year or $750 per month

These figures represent the total residential bill including municipal, education, and city building fund components. Individual bills will vary based on specific assessed values, any applicable rebates, and whether the property qualifies for special programs.

The City of Toronto provides an online property tax calculator at toronto.ca/taxes that allows homeowners and prospective buyers to calculate estimated bills based on specific assessed values with current year rates applied.

| Assessed Property Value | Est. Annual Tax (2026) | Est. Monthly Equivalent | Typical Property Type |

|---|---|---|---|

| $600,000 | ~$3,598 | ~$300 | Condo apartment, small townhouse |

| $800,000 | ~$4,798 | ~$400 | Semi-detached, mid-range townhouse |

| $1,000,000 | ~$5,997 | ~$500 | Detached home, South Etobicoke |

| $1,200,000 | ~$7,196 | ~$600 | Larger detached, premium areas |

| $1,500,000 | ~$8,996 | ~$750 | Premium detached, Kingsway South |

| $2,000,000 | ~$11,994 | ~$1,000 | Luxury estate, The Kingsway |

Property Tax Assessment in Etobicoke: How MPAC Determines Your Value

The assessed value that Toronto uses to calculate your property tax bill is determined by the Municipal Property Assessment Corporation — the independent provincial body responsible for valuing all properties in Ontario. Understanding how MPAC arrives at your assessed value is essential for determining whether your bill is correct and whether a reassessment or appeal is warranted.

MPAC’s Current Value Assessment (CVA) is the estimated value of your property as of a specific valuation date. MPAC is legislatively required to reassess all properties in Ontario on a four-year cycle. The most recent province-wide reassessment used January 1, 2016 as its valuation date. Ontario announced that the next province-wide reassessment would use a 2022 valuation date, but the implementation timeline has been subject to legislative review. As of 2026, many properties in Etobicoke continue to be assessed based on values that may not fully reflect current market conditions.

What this means practically for Etobicoke homeowners: Properties that were assessed during a period of lower market values may have CVA figures significantly below current market prices, resulting in lower tax bills than a fully current assessment would produce. Conversely, properties assessed at or near market peak values carry higher CVA figures and correspondingly higher annual bills.

How MPAC determines your assessed value: MPAC uses a mass appraisal methodology that considers comparable sales, property characteristics including lot size, gross floor area, construction quality, age, and location. MPAC sends property owners a Property Assessment Notice when reassessment occurs, providing the assessed value and a comparison to similar properties in the area.

The disclosure and appeal process: Every property owner in Ontario has the right to review their assessment and challenge it through the Assessment Review Board if they believe it is incorrect. The process begins with a Request for Reconsideration (RfR) submitted directly to MPAC — a free administrative review that must be completed before a formal ARB appeal can proceed. The Government of Ontario’s MPAC portal provides current assessment data and the tools required to begin a reconsideration request.

Property Tax Assessment Dispute: When and How to Challenge Your Bill

For Etobicoke homeowners who believe their MPAC assessment is too high relative to comparable properties — a situation that creates overpayment of property tax — the dispute process provides a structured path to correction.

Circumstances that may justify challenging an assessment:

- Your assessed value is significantly higher than the selling prices of comparable recently sold properties in your Etobicoke neighborhood

- Your property has characteristics that MPAC’s records do not correctly reflect — incorrect square footage, incorrect number of bathrooms, or features that do not exist

- Comparable neighboring properties with similar characteristics carry materially lower assessed values without a reasonable explanation

- Your property has sustained damage, functional obsolescence, or other value-reducing factors not reflected in the assessment

The two-stage challenge process:

Stage 1 — Request for Reconsideration (RfR): Submit a formal RfR to MPAC within 120 days of receiving your Property Assessment Notice. MPAC reviews the assessment against comparable sales data and property records. This is a free process and the mandatory first step before any formal appeal. MPAC typically responds within 180 days with either a revised assessment or a confirmation of the original figure.

Stage 2 — Assessment Review Board (ARB) Appeal: If the RfR does not produce a satisfactory result, property owners can appeal to the Assessment Review Board within the legislatively defined deadline. ARB appeals involve a formal hearing process and may benefit from professional representation, particularly for higher-value properties where the tax savings from a successful appeal justify the cost of professional advocacy.

For newcomers to Etobicoke arriving from other provinces who are unfamiliar with Ontario’s assessment system, understanding these rights before making a purchase helps ensure you are not overpaying from the first year of ownership. The guide to Etobicoke real estate for newcomers covers the full purchase and ownership context for those new to Ontario’s property system.

Etobicoke Property Tax vs. Mississauga: An Honest Comparison

For buyers comparing residential addresses on either side of the Etobicoke-Mississauga boundary, the property tax comparison is one of the most financially significant differences between the two municipalities — and one that is consistently underweighted in relocation decision-making.

Mississauga’s 2026 residential property tax rate is approximately 0.804% of assessed value — meaningfully higher than Toronto’s residential rate of approximately 0.5997%. This difference is not trivial over the lifetime of homeownership.

On a property assessed at $1,000,000:

- Etobicoke (Toronto rate): approximately $5,997 per year

- Mississauga: approximately $8,040 per year

- Annual difference: approximately $2,043

- 10-year cumulative difference: approximately $20,430

On a property assessed at $1,500,000:

- Etobicoke (Toronto rate): approximately $8,996 per year

- Mississauga: approximately $12,060 per year

- Annual difference: approximately $3,064

- 10-year cumulative difference: approximately $30,640

This tax differential is one of the most compelling financial arguments for choosing an Etobicoke address over a comparable Mississauga property — and it persists as a year-over-year advantage as long as the rate differential between Toronto and Mississauga is maintained. For buyers who are conducting a genuine South Etobicoke vs North Etobicoke cost comparison alongside the Etobicoke-Mississauga comparison, the Toronto rate advantage applies equally to both parts of the district.

| Municipality | 2026 Residential Tax Rate | Tax on $800K Assessment | Tax on $1.2M Assessment | Tax on $1.5M Assessment |

|---|---|---|---|---|

| Etobicoke (Toronto) | ~0.5997% | ~$4,798 | ~$7,196 | ~$8,996 |

| Mississauga | ~0.804% | ~$6,432 | ~$9,648 | ~$12,060 |

| Brampton | ~1.01% | ~$8,080 | ~$12,120 | ~$15,150 |

| Vaughan | ~0.68% | ~$5,440 | ~$8,160 | ~$10,200 |

| Markham | ~0.632% | ~$5,056 | ~$7,584 | ~$9,480 |

Understanding Your Toronto Tax Bill: What Every Line Item Means

When your annual property tax bill arrives from the City of Toronto, understanding each component helps you confirm accuracy, plan payments, and understand where your tax dollars are directed.

Current Value Assessment (CVA) — the MPAC-determined value of your property. This is the base number from which all calculations flow. If this number looks incorrect, the reconsideration process described above is the path to correction.

Phased-in Assessment Value — where a property’s CVA increased significantly from the previous assessment period, Ontario legislation allows the increase to be phased in over four years to prevent sudden large tax increases. Your tax bill may show both the full CVA and the phased-in value currently being used for calculation.

Municipal Tax Rate — the City of Toronto’s residential rate applied to your phased-in assessment value. This produces the municipal component of your bill.

Education Tax Rate — the provincial education levy rate applied to your assessment value. This portion is remitted to the Province of Ontario for distribution to school boards.

City Building Fund Levy — Toronto’s dedicated infrastructure fund levy, shown as a separate line item. This was introduced in 2020 and is increased annually to fund transit and housing infrastructure.

Tax Installment Schedule — your bill shows the installment due dates and amounts for the current year. Most Toronto residential property owners pay in installments rather than a single annual payment.

Outstanding Balance — any previous year amounts outstanding will appear on the current bill. Unpaid property tax in Toronto accrues interest at a legislatively determined rate.

Property Tax Payment Deadlines in Toronto: Interim and Final Bills

The City of Toronto issues property tax bills twice per year — the Interim Bill in the first half of the year and the Final Bill in the second half. Understanding this structure and the specific deadlines prevents late payments and the penalties they carry.

The Interim Tax Bill: The Interim Bill is issued in January or February each year and covers the first half of the tax year. It is based on 50% of the previous year’s property tax amount rather than the current year’s rate — the current year’s rate has not yet been finalized when the Interim Bill is issued. The Interim Bill is typically paid in three installments:

- First installment: Due in March (typically the third Thursday of March)

- Second installment: Due in April (typically the third Thursday of April)

- Third installment: Due in June (typically the third Thursday of June)

The Final Tax Bill: The Final Bill is issued in May or June after the current year’s tax rate has been approved through the City of Toronto budget process. It reflects the full current year tax calculation and credits the Interim Bill payments already made. Any remaining balance is paid in three additional installments:

- Fourth installment: Due in July (typically the third Thursday of July)

- Fifth installment: Due in September (typically the third Thursday of September)

- Sixth installment: Due in November (typically the third Thursday of November)

Late payment penalties: The City of Toronto charges a 1.25% penalty on any unpaid taxes on the first day after the due date. An additional 1.25% interest charge applies on the first day of each subsequent month that the amount remains unpaid. For a $5,000 installment, the first month’s late penalty is $62.50 — a meaningful cost that compounds quickly if multiple installments fall into arrears.

For new Etobicoke homeowners arriving from other provinces who are unfamiliar with Ontario’s property tax billing cycle, setting calendar reminders for all six installment dates immediately upon receiving the first tax bill eliminates the most common and entirely preventable source of late payment penalties.

How to Pay Property Tax in Toronto: Every Available Method

The City of Toronto provides multiple payment channels that accommodate different preferences and lifestyles. Understanding every option allows homeowners to choose the method that best fits their banking arrangements and payment habits.

Online banking — the most common method: Most major Canadian banks allow Toronto property tax payments through online banking using the tax account number printed on your bill as the payee account. Set up City of Toronto Property Tax as a payee once, then schedule payments for each installment due date. This method provides automatic payment records within your banking statement and allows scheduling payments in advance.

Pre-authorized payment plan — the most convenient method: Toronto’s pre-authorized tax payment programs allow homeowners to authorize automatic bank account deductions on installment due dates. Three program options are available:

- Monthly payment plan — equal monthly payments spread across the year, debited on the 15th of each month

- Installment payment plan — payments on the six standard installment dates

- Online banking payment plan — similar to the installment plan but initiated through online banking rather than city authorization

Enrollment in the pre-authorized plan eliminates the risk of missed payments entirely and is the most recommended approach for homeowners who want to set and forget their property tax obligations.

In-person payment: Payments can be made in person at any Toronto Civic Centre, including the Etobicoke Civic Centre at 399 The West Mall. Payment by cheque, debit, or cash is accepted at civic centre cashier windows during business hours.

By mail: Cheques payable to the Treasurer, City of Toronto, can be mailed to the address on the tax bill. Allow sufficient transit time before the due date to prevent late payment. Post-dated cheques are accepted.

Mortgage lender payment: Many mortgages in Canada include property tax collection through the regular mortgage payment — the lender collects a monthly property tax installment with the mortgage payment and remits it to the City of Toronto on the homeowner’s behalf. Confirm with your lender whether your mortgage includes this arrangement, as it eliminates the need for separate property tax management entirely.

Property Tax Rebates and Relief Programs for Etobicoke Homeowners

The City of Toronto and the Province of Ontario both offer programs that reduce property tax obligations for qualifying homeowners. Understanding these programs before finalizing a purchase can reveal annual savings that affect the total carrying cost calculation.

Toronto’s Assessment Phase-In Program: As noted earlier, Toronto phases in assessment increases over four years to prevent sudden large tax jumps. For properties that experienced significant CVA increases in the most recent reassessment, the phase-in period provides meaningful temporary relief.

Ontario Senior Homeowners’ Property Tax Grant: Ontario residents aged 64 and over who owned and occupied their principal residence in Ontario can receive a grant of up to $500 annually to help offset property tax costs. The grant is claimed through the Ontario personal income tax return and requires no separate property tax application. For senior residents being supported by senior moving services transitioning to an Etobicoke address, awareness of this grant from the first year of ownership ensures the benefit is not overlooked.

Ontario Energy and Property Tax Credit (OEPTC): The OEPTC provides relief for eligible low-to-moderate income Ontario residents through the Ontario personal income tax system. The property tax component of the credit provides up to $346 per year for eligible non-seniors and up to $521 for eligible seniors. The credit is income-tested and claimed through the annual tax return.

First-Time Purchaser Rebate: Buyers who have never previously owned a home anywhere in the world — or whose spouse or domestic partner has not — may qualify for a Toronto land transfer tax rebate of up to $4,475 on the purchase of a home in Toronto (including Etobicoke). While technically a land transfer tax benefit rather than a property tax rebate, it represents a significant one-time financial benefit for eligible first-time buyers that directly affects the total cost of purchasing in Etobicoke.

Vacancy rebate and tax deferral programs: Commercial and multi-residential property owners have access to vacancy rebate programs that do not apply to standard residential homeowners. However, homeowners experiencing genuine financial hardship may qualify for property tax deferral programs — contact the City of Toronto Revenue Services at toronto.ca/taxes for current program availability.

Property Tax Increases in Etobicoke: Historical Trends and What to Budget For

For buyers making long-term financial plans based on today’s tax rates, understanding the historical trend of Toronto property tax increases is essential for accurate multi-year budgeting.

The City of Toronto has implemented the following residential property tax rate increases in recent years:

- 2024: 9.5% increase (the largest single-year increase in decades, driven by post-pandemic budget pressures)

- 2025: 6.9% increase

- 2026: 6.9% increase

These increases have compounded significantly for Etobicoke homeowners over the three-year period. A homeowner paying $5,000 in property tax in 2023 was paying approximately $5,975 by 2026 — a $975 or 19.5% increase over three years on the same property.

Toronto’s budget pressures reflect the city’s ongoing capital infrastructure requirements — particularly the transit network expansion funded through the City Building Levy — and the inflationary pressures on city service delivery costs that are consistent with broader Ontario municipal trends.

For prospective Etobicoke buyers budgeting annual property tax, the prudent approach is to apply a conservative 4–7% annual increase assumption to current tax bills when projecting 5–10 year carrying costs. This range reflects both recent actual increases and the probability of some moderation as capital program spending normalizes.

For families comparing the full cost of living in Etobicoke in 2026 and evaluating how to save money when moving to a new property, the multi-year tax projection should be a standard component of the financial analysis alongside mortgage carrying costs and utility estimates.

Property Tax Implications by Etobicoke Neighborhood

Etobicoke’s diverse range of neighborhoods creates significant variation in actual annual property tax bills — not because different neighborhoods face different rates (Toronto’s rate is uniform across the city) but because assessed values vary enormously between the district’s most and least expensive communities.

The Kingsway and Kingsway South: Among the highest-assessed neighborhoods in Etobicoke, with detached homes regularly carrying CVA figures of $1,500,000–$2,500,000 and annual tax bills correspondingly in the $9,000–$15,000 range. For families evaluating the best neighborhoods in Etobicoke, The Kingsway’s premium on both purchase price and annual tax bill reflects its positioning as the district’s most prestigious residential community.

Mimico and Humber Bay Shores: Condo apartments in the Humber Bay Shores cluster carry assessed values of $500,000–$900,000 depending on unit size and floor, producing annual bills in the $3,000–$5,400 range. For the full picture of moving to Mimico and what the complete cost of living there involves, the property tax range in this community is one of its more accessible attributes.

Long Branch and Alderwood: Detached homes in these South Etobicoke communities carry assessed values typically in the $800,000–$1,200,000 range, producing annual bills of approximately $4,800–$7,200. These communities represent the most affordable neighborhood access points in South Etobicoke, where property tax bills reflect the more accessible price points.

Rexdale and West Humber-Clairville: North Etobicoke’s more affordable communities feature lower assessed values — detached homes often carrying CVA figures of $700,000–$950,000 — and correspondingly lower annual bills in the $4,200–$5,700 range. For buyers seeking the cheapest places to live in Etobicoke, North Etobicoke’s lower assessment base translates directly into lower annual property tax bills that reduce total homeownership costs.

Islington Village and Edenbridge-Humber Valley: Mid-range central Etobicoke communities where detached home CVA figures typically range from $1,000,000–$1,600,000, producing annual tax bills of $6,000–$9,600 depending on specific property characteristics.

The Toronto Property Tax Calculator: How to Use It Before You Buy

The City of Toronto’s online property tax calculator, available at toronto.ca/taxes, is one of the most practical pre-purchase research tools available to prospective Etobicoke buyers. Using the calculator with the MPAC-assessed value of a specific property under consideration — available through the MPAC’s About My Property portal — provides an accurate annual tax estimate before any purchase commitment.

How to use the calculator effectively:

- Obtain the current MPAC assessed value of the property from your real estate agent, the MPAC portal, or the seller’s most recent tax bill

- Enter the assessed value into the City of Toronto’s tax calculator using the current year’s residential rates

- Note the total annual figure and divide by 12 for the monthly equivalent to incorporate into your total housing cost budget

- Apply a 5% annual increase assumption and recalculate for years 3, 5, and 10 to understand the long-term trajectory of this carrying cost

For buyers comparing multiple properties across different Etobicoke neighborhoods — or comparing Etobicoke properties against options in Mississauga, North York, or Vaughan — running the calculator for each address on the shortlist produces directly comparable annual tax figures that allow genuine apples-to-apples financial comparison.

Frequently Asked Questions

What is the property tax rate in Etobicoke in 2026?

Etobicoke falls within the City of Toronto and pays Toronto’s residential property tax rate of approximately 0.5997% of the MPAC current value assessment for 2026. This rate represents a 6.9% increase from the 2025 rate and includes the municipal levy, education levy, and city building fund components. The City of Toronto’s online calculator at toronto.ca/taxes provides specific bill estimates for any assessed value.

How is Etobicoke property tax calculated?

Etobicoke property tax is calculated by multiplying the MPAC current value assessment of your property by Toronto’s total residential tax rate. For a property assessed at $1,000,000, the 2026 tax bill is approximately $5,997 per year. The assessment is determined by MPAC through comparable sales analysis and property characteristic evaluation, not by the purchase price or current market value.

Is property tax in Etobicoke lower than Mississauga?

Yes — significantly. Etobicoke pays Toronto’s residential rate of approximately 0.5997%, while Mississauga’s 2026 residential rate is approximately 0.804%. On a $1,000,000 assessed property, this difference produces an annual Etobicoke saving of approximately $2,043 over Mississauga — a cumulative advantage of over $20,000 across ten years on the same property.

When are property taxes due in Etobicoke?

City of Toronto property taxes are paid in six installments — three for the Interim Bill (typically March, April, and June) and three for the Final Bill (typically July, September, and November). The City charges a 1.25% penalty on unpaid amounts the day after each due date, with an additional 1.25% monthly interest on continuing arrears.

How do I pay my Etobicoke property tax bill?

Payment can be made through online banking using the tax account number as the payee, through Toronto’s pre-authorized payment plan, in person at Etobicoke Civic Centre at 399 The West Mall, or by mail. The pre-authorized plan is the most convenient method — it automatically deducts the correct amount on each due date, eliminating the risk of missed payments.

Etobicoke Property Tax Is One of the Most Valuable Financial Steps You Can Take Before Making Your Move

Etobicoke property tax is not a peripheral consideration in the home buying and relocation decision — it is a significant annual carrying cost that persists for as long as you own your property and increases at a rate that compounds meaningfully over the years. Understanding how your assessed value is determined, what the 2026 rate produces on specific property values, how the Etobicoke tax rate compares to Mississauga and other GTA municipalities, and exactly when and how to pay gives you the complete financial picture that sound homeownership decisions require. Combined with the broader Etobicoke cost of living analysis for 2026, the property tax picture confirms what the data consistently shows — Etobicoke delivers one of the most favorable total cost of ownership profiles available in the Greater Toronto Area, with a residential tax rate that is meaningfully below most comparable municipalities in the region. When you are ready to make your move, Metropolitan Movers Etobicoke is here to handle every detail — from residential moving services and packing support to storage solutions and long-distance relocations from anywhere in Canada — with 15+ years of experience ensuring your transition to your new Etobicoke home is as seamless as the financial advantages that brought you here.

dd