Navigating Etobicoke real estate for newcomers is one of the most consequential financial decisions you will make in your first years in Canada — and it is also one of the most confusing. The rules are different here. The mortgage system works differently than what you may be accustomed to. The terminology — land transfer tax, MPAC assessment, rent-geared-to-income, FHSA, amortization period — can feel like a second language on top of the one you are already learning. And the stakes are enormous: choosing the right neighbourhood, the right housing type, and the right timing can mean the difference between building genuine wealth and stretching your budget past its breaking point. This guide, assembled by the relocation team at Metropolitan Movers Etobicoke, walks through every step of the newcomer housing journey in Etobicoke — from your first temporary rental through to homeownership — so you can make decisions rooted in knowledge rather than guesswork.

Etobicoke occupies Toronto’s entire western flank, stretching from Lake Ontario in the south to Steeles Avenue in the north, from the Humber River in the east to the Etobicoke Creek and Highway 427 in the west. It is home to more than 365,000 residents from backgrounds spanning every continent, and its multicultural fabric is one of the primary reasons newcomers choose this part of the city. The Rexdale and Mount Olive corridors in north Etobicoke are among the most culturally diverse communities in the entire GTA, with established South Asian, Somali, Caribbean, and Filipino populations that provide social infrastructure, places of worship, specialty grocery stores, and community networks that ease the transition to Canadian life. The waterfront communities of Mimico, Long Branch, and Humber Bay Shores attract newcomers seeking a more urban lifestyle with lake access and rapid transit to downtown.

Whether you are a permanent resident who arrived last month, a work permit holder settling into your first Canadian job, or a family that has been in Canada for a few years and is now ready to transition from renting to owning, this resource covers every angle of the journey. If you are already planning the physical move into your first Etobicoke home, understanding what a residential relocation in Etobicoke actually involves — from building logistics to neighbourhood access — will prevent costly surprises on moving day.

Etobicoke Real Estate Market Forecast 2026: What Newcomers Need to Understand Before Entering

Before committing any money to housing, every newcomer should understand where the Etobicoke real estate market sits right now and where it is likely heading over the next twelve to eighteen months.

The Current Market Snapshot

The Etobicoke real estate landscape in 2026 is dynamic. While price growth has moderated compared to the frenzy of 2020 through 2022, buyer opportunities and value exist across neighbourhoods and housing types. In 2026, Etobicoke’s market dynamics reflect a blend of affordability challenges and lifestyle appeal — a combination that creates both risk and opportunity for newcomers entering the market.

Across the broader GTA, home sales in February 2026 declined roughly 6.3 percent year-over-year, and new listings dipped as well. There is substantial pent-up demand in the GTA ownership market, with more than 100,000 buyers holding off on making a home purchase. Buyers are waiting for selling prices to level off and for positive economic signals. Once those signals arrive, there could be substantial momentum driving home sales in the second half of 2026 and into 2027.

For newcomers, the current moment presents a strategic window. Competition among buyers is lower than it was during the pandemic boom. Properties are sitting on the market longer — 54 days on average across Toronto in February 2026, up from 43 days a year earlier. And the sale-to-list price ratio has dropped to approximately 97 percent, meaning homes are selling for roughly 3 percent below their asking price. These are favourable conditions for patient, prepared newcomer buyers. Families relocating into Etobicoke from another province or country should use this transition period to explore neighbourhoods in person before committing to a purchase.

What the Forecast Suggests

Major real estate organizations forecast a measured recovery in sales and largely flat to modestly rising prices through 2026. However, some analysts expect prices to decline further in certain segments — particularly condos and luxury properties — before more buyers are drawn off the sidelines. For Ontario and British Columbia specifically, 2026 will likely bring continued price pressure in major metro areas, though the erosion should be limited mostly to condos and the luxury tier.

The Bank of Canada has maintained its policy rate at 2.25 percent as of early 2026 — a level considered neutral by most economists. This represents a dramatic reduction from the 5.0 percent peak in 2022-2023, and borrowing conditions have improved substantially for anyone applying for a mortgage today.

The practical takeaway for newcomers: this is not a market where you need to rush. Take the time to build your credit, save your down payment, and understand your neighbourhood options. The urgency that characterized the 2021-2022 market does not exist in 2026.

First-Time Home Buyer Programs in Ontario: Every Incentive Newcomers Can Access

One of the most common misconceptions among newcomers is that they are not eligible for first-time home buyer programs. In reality, permanent residents and even some work permit holders qualify for the same incentives available to Canadian-born buyers — and in some cases, newcomer-specific programs provide additional support.

The First Home Savings Account (FHSA)

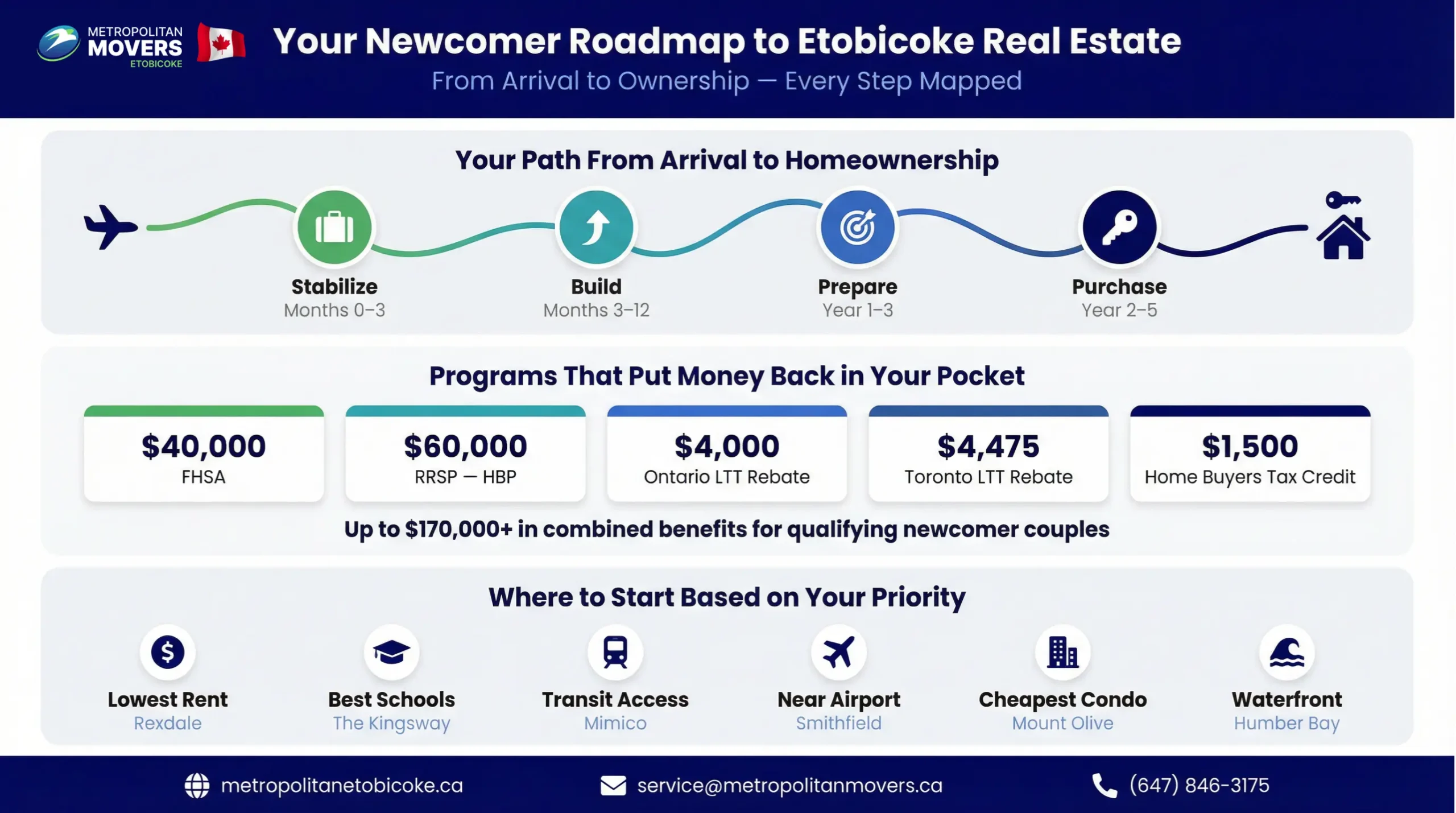

The FHSA is a tax-advantaged registered savings plan that combines the best features of an RRSP and a TFSA. Contributions are tax-deductible (like an RRSP), and withdrawals used for a qualifying home purchase are completely tax-free (like a TFSA). You can contribute up to $8,000 per year, with a lifetime maximum of $40,000. Unlike the RRSP Home Buyers’ Plan, you do not have to repay the funds you withdraw from the account. This is arguably the single most powerful savings tool available to newcomers who plan to buy within the next three to five years.

The RRSP Home Buyers’ Plan (HBP)

The HBP allows first-time buyers to withdraw up to $60,000 from their Registered Retirement Savings Plan tax-free to put toward a home purchase. If buying with a partner who also qualifies, you can withdraw up to $120,000 combined. The withdrawn amount must be repaid over 15 years, starting in the second year after the withdrawal. You can use both the FHSA and HBP for the same home purchase, meaning maximum combined savings of $100,000 per person or $200,000 for couples.

Land Transfer Tax Rebates for First-Time Buyers

Ontario provides a land transfer tax rebate of up to $4,000 for qualifying first-time buyers. In Toronto specifically — which includes all of Etobicoke — first-time buyers are also eligible for a separate municipal land transfer tax rebate of up to $4,475. Combined, these rebates can recover up to $8,475 in closing costs. To qualify, you must have never owned a home anywhere in the world, must be at least 18 years old, and must occupy the property as your principal residence within nine months of purchase. If you are buying your first Etobicoke home and claim both rebates, the savings can cover a significant portion of your closing costs.

The First-Time Home Buyers’ Tax Credit (HBTC)

Eligible first-time buyers can claim up to $10,000 on their federal tax return, resulting in a $1,500 tax reduction. This credit helps offset closing costs like legal fees, home inspections, and title insurance.

Extended Amortization for First-Time Buyers

As of December 2024, first-time homebuyers in Canada can access 30-year amortization periods on insured mortgages, extending the standard 25-year maximum. This applies to buyers with a down payment of less than 20 percent who require mortgage insurance. The extended amortization reduces monthly mortgage payments, improving affordability and helping more Canadians qualify for home financing. Additionally, the cap for insured mortgages has been raised from $1 million to $1.5 million, meaning more Etobicoke properties fall within the insured mortgage threshold.

| Program | Maximum Benefit | Key Requirement |

|---|---|---|

| First Home Savings Account (FHSA) | $40,000 lifetime (tax-free) | Canadian resident, under 40 at account opening |

| RRSP Home Buyers’ Plan (HBP) | $60,000 per person ($120K couple) | Must repay over 15 years |

| Ontario Land Transfer Tax Rebate | Up to $4,000 | Never owned a home anywhere in the world |

| Toronto Municipal LTT Rebate | Up to $4,475 | Buying in Toronto; principal residence within 9 months |

| Home Buyers’ Tax Credit (HBTC) | $1,500 tax savings | Claimed on federal tax return for year of purchase |

| 30-Year Amortization (Insured) | Lower monthly payments | First-time buyer or new build; less than 20% down |

| GST/HST New Housing Rebate | Varies by price | Purchasing new build from builder |

When combining FHSA, HBP, and both land transfer tax rebates, a qualifying newcomer couple could access up to $200,000 in tax-advantaged savings plus $8,475 in closing cost rebates plus $3,000 in federal tax credits. These programs exist specifically to lower the barriers for first-time buyers — and newcomers who are permanent residents qualify for every single one.

Etobicoke Mortgage Rates for New Immigrants: How Newcomer Financing Actually Works

One of the biggest myths newcomers face is that they cannot qualify for a Canadian mortgage without years of credit history and employment. The reality is significantly more accessible than most people expect.

Newcomer Mortgage Programs at Major Banks

Canada’s major mortgage insurers — CMHC, Sagen, and Canada Guaranty — all offer specialized programs to help newcomers access financing for their first home. These insurer-backed programs are available through most major Canadian banks and enable permanent residents to qualify for a mortgage with as little as 5 percent down, even with limited Canadian credit history, provided they have been in Canada within the past five years and have at least three months of full-time Canadian employment.

The eligibility framework works as follows:

- Permanent residents (arrived within 5 years): Minimum 5 percent down payment with mortgage insurance; no Canadian credit history required if other documentation is provided

- Permanent residents (no Canadian credit): Some lenders offer a 35 percent down payment option that waives the need for mortgage insurance entirely, eliminating the credit history requirement

- Work permit holders (arrived within 2 years): Eligible for newcomer mortgage programs with valid work permits and at least 3 months of Canadian employment

- International credit history: Many Canadian lenders accept international credit reports as supporting documentation when Canadian credit is limited

A credit score of 660 or higher is preferred for the most favourable rates, but programs exist for those still building their Canadian credit. Building your credit proactively by opening and using a Canadian credit card, paying all bills on time, and maintaining consistent employment strengthens your mortgage application significantly.

Current Mortgage Rate Environment

As of early 2026, the Bank of Canada’s policy rate sits at 2.25 percent — well below the 5.0 percent peak reached during the tightening cycle of 2022-2023. Some analysts forecast a possible gradual rate increase later in 2026, but the current environment is substantially more favourable for borrowers than anything seen in the past three years. Fixed five-year mortgage rates are generally available in the 4.0 to 5.0 percent range, while variable rates fluctuate near the prime rate.

What Newcomers Should Budget Beyond the Mortgage Payment

Your total monthly housing costs must stay within specific ratios to qualify for a mortgage. Total monthly housing costs — including mortgage, property taxes, and utilities — should not exceed 39 percent of your gross income, and total debt payments must stay under 44 percent. These ratios apply regardless of your immigration status.

For newcomers moving into their first owned home in Etobicoke, budgeting for the full picture — not just the mortgage payment — is critical. Property taxes, condo maintenance fees, home insurance, and utilities can add $500 to $1,500 per month on top of your mortgage.

New Development Condos in Etobicoke: Fresh Inventory for Newcomer Buyers

Pre-construction and newly built condominiums represent a compelling option for newcomers entering the Etobicoke market. They offer modern designs, energy-efficient building systems, contemporary amenities, and structured payment plans that can align well with a newcomer’s savings timeline.

The Current Development Landscape

Etobicoke’s new condo market is active, with more than 60 pre-construction and recently completed projects currently available or in planning stages across the former municipality. The pricing for condos in Etobicoke is often more competitive than in downtown Toronto, making it a favourable choice for buyers seeking affordability without sacrificing convenience.

The cost per square foot for new condos in Etobicoke typically ranges from $700 to $1,200, depending on the specific development, neighbourhood, and finish level. The average pre-construction appreciation rate in Etobicoke over the past decade has been approximately 8 percent annually — though past performance is never a guarantee of future returns, especially in a market that is currently recalibrating.

Key New Developments by Price Tier

Entry-level (from the mid-$400,000s):

- Kipling Station Condos at 5251 Dundas Street West — directly adjacent to Kipling subway station, with pricing from the mid-$400,000s and 2026 occupancy

- The 9Hundred Condos at 900 The East Mall — one to three-bedroom units from $440,000 to $880,000 with 2026 occupancy

- Queensway corridor developments — multiple projects along The Queensway from the mid-$400,000s to low $600,000s

Mid-range (from the mid-$500,000s to $900,000s):

- Arcadia District at 60 Fieldway Road — from the mid-$500,000s with 2027 move-in

- Westshore at Long Branch — townhome development by a major builder from the high $500,000s

- Multiple projects along Bloor Street West and the Islington City Centre corridor

Premium ($900,000+):

- Edenbridge Kingsway Condos — luxury development from $2,100,000 in The Kingsway neighbourhood

- Waterfront developments in Humber Bay Shores and Mimico — premium towers from $700,000 to $1,500,000+

Newcomers purchasing pre-construction condos benefit from structured deposit schedules — typically 15 to 20 percent of the purchase price spread over 12 to 24 months — which provides time to build savings after arrival. However, pre-construction purchases carry risks including construction delays, market value changes between purchase and occupancy, and the potential for higher-than-expected maintenance fees. When your new condo is ready for occupancy, understanding the building’s move-in procedures — elevator booking, insurance certificates, and loading dock scheduling — is essential for a smooth transition.

Short Term Rentals for Newcomers in Etobicoke: Where to Land First

Most newcomers do not buy a home immediately upon arrival. The first housing step is almost always a rental — often a short-term arrangement while you establish employment, build credit, learn the city, and determine which neighbourhood fits your long-term needs.

Furnished Short-Term Options

Etobicoke offers several categories of short-term rental housing for newcomers:

- Corporate furnished apartments — Available in Humber Bay Shores, Mimico, and along The Queensway, these units are typically rented on one to six-month terms and come fully furnished with kitchen supplies, linens, and internet. Pricing ranges from $2,200 to $4,000 per month for a one-bedroom unit.

- Month-to-month furnished rooms — North Etobicoke neighbourhoods near Humber College offer furnished rooms in shared houses from $800 to $1,250 per month, with utilities and internet typically included. These are popular with international students and newcomers during their first months.

- Basement apartments with flexible terms — Homeowners in Rexdale, Smithfield, and Thistletown frequently offer month-to-month basement rentals from $1,100 to $1,500, often furnished or semi-furnished, providing a private living arrangement while you search for permanent housing.

- Extended-stay hotels and suites — Located near Pearson Airport and along the Highway 427 corridor, these provide the most flexible terms but at the highest per-night cost. Budget $100 to $180 per night, or $2,500 to $4,500 per month.

For newcomers arriving with household goods shipped from their home country, coordinating the delivery timeline with your short-term rental arrangement is critical. If your belongings arrive before your permanent home is ready, secure temporary storage bridges the gap without forcing you to rush your housing decision.

The Best Neighbourhoods for Newcomer Short-Term Rentals

- Rexdale-Kipling and Smithfield — Most affordable options; strong newcomer community networks; proximity to Humber College and Pearson Airport

- Islington-City Centre West — Direct subway access at Islington station; mid-range pricing; walkable commercial corridor

- Mimico and Humber Bay Shores — Waterfront lifestyle; higher pricing but abundant furnished condo inventory; GO Transit access to downtown

Leasing Process for New Residents in the GTA: What Every Newcomer Must Know

The leasing process in Ontario operates under the Residential Tenancies Act, which provides significant protections for tenants — but also includes rules and requirements that newcomers may not be familiar with.

How Renting Works in Ontario

- First and last month’s rent — Landlords can legally require first and last month’s rent at the time of signing. No other deposits — including security deposits or damage deposits — are permitted under Ontario law.

- Rent control — Buildings first occupied before November 15, 1991 are subject to the provincial rent increase guideline, which caps how much a landlord can raise rent each year. Buildings occupied after that date are not subject to this cap, meaning landlords can increase rent by any amount with proper notice.

- Standard Ontario lease — All residential tenancies in Ontario must use the province’s Standard Lease form. Landlords who try to use a different form are not in compliance with the law.

- Notice requirements — Landlords must provide 90 days written notice of a rent increase, and increases can only happen once every 12 months.

- No discrimination — The Ontario Human Rights Code prohibits landlords from refusing to rent based on race, ancestry, place of origin, citizenship, ethnic origin, family status, or receipt of public assistance. Newcomers are protected under all of these grounds.

Documentation Newcomers Typically Need for a Rental Application

Most landlords in the GTA will request the following when you apply for a rental:

- Proof of employment (employment letter, pay stubs, or employment contract)

- Proof of income (bank statements showing regular deposits)

- Photo identification (passport, PR card, or Ontario photo card)

- References (previous landlords if available; employer references as an alternative)

- Credit check authorization (newcomers with no Canadian credit can often substitute bank statements or international credit documentation)

If you are moving from a short-term rental into your first permanent Etobicoke apartment, the transition is smoother when you have your documentation organized in advance. Many landlords in competitive rental markets make decisions quickly, and having your application package ready can be the difference between securing a unit and losing it.

Tenant Rights Newcomers Should Know

Ontario’s Residential Tenancies Act protects tenants from illegal evictions, unauthorized entry, and above-guideline rent increases in controlled buildings. The Ontario government’s rental housing page provides the full text of tenant rights and responsibilities, and newcomers should review this resource before signing any lease. If disputes arise, the Landlord and Tenant Board provides a resolution process that does not require legal representation.

Etobicoke Settlement Services and Housing Help: Free Support for Newcomers

Navigating housing as a newcomer does not have to be a solo effort. Etobicoke is home to multiple settlement organizations funded by Immigration, Refugees and Citizenship Canada (IRCC) that provide free, multilingual support specifically designed to help newcomers find, secure, and maintain housing.

Key Settlement Organizations Serving Etobicoke

- COSTI Immigrant Services — One of the largest settlement agencies in Ontario, COSTI provides newcomer referrals to community resources including housing, health, education, and legal facilities. Their services include help completing government documents, orientation sessions on landlord-tenant rights, budgeting assistance, and interpretation services in multiple languages.

- Albion Neighbourhood Services — Etobicoke Housing Help Centre — Located in north Etobicoke, this centre provides direct housing search assistance, application support, and connections to subsidized and affordable housing programs.

- Newcomer Women’s Services Toronto — Offers settlement services tailored for newcomer women, including housing assistance, English language classes, crisis counselling, and community connection programs.

- YMCA Newcomer Information Centre — Serves as a first-stop resource for immigrants and refugees in the GTA, providing information and referrals on employment, education, language classes, health, housing, and settlement planning.

These organizations help with practical tasks like understanding lease agreements, completing applications for subsidized housing, navigating the Rent-Geared-to-Income waitlist, and connecting newcomers with affordable housing opportunities that are not advertised on mainstream rental platforms.

An important policy change for 2026: starting April 1, 2026, economic class permanent residents can only access federally funded newcomer settlement services for a limited time. This means registering with settlement agencies early — ideally within your first months in Canada — is more important than ever. The IRCC settlement services directory helps you find organizations nearest to your Etobicoke address.

For newcomers who are preparing to relocate from temporary housing into a permanent rental or purchased home, settlement workers can sometimes help coordinate timing and documentation to align with your move date.

Etobicoke Neighbourhoods Mapped by Newcomer Priority

Different newcomers have different priorities, and Etobicoke’s neighbourhood diversity means there is a strong match for virtually every situation. Here is a quick-reference guide based on the factors newcomers most commonly prioritize:

- Lowest possible rent (shared housing, basement apartments): Rexdale-Kipling, Mount Olive-Silverstone-Jamestown, Smithfield, Thistletown

- Most affordable home purchase entry point: Mount Olive (condos from under $400,000), Rexdale-Kipling, West Humber-Clairville

- Strongest newcomer community networks: Rexdale, Mount Olive, Islington Village — established multicultural communities with places of worship, ethnic grocers, and community organizations

- Best transit access for downtown commuters: Mimico and Long Branch (GO Transit, 13-minute ride to Union Station), Islington-City Centre West (subway access)

- Airport employment zone proximity: Smithfield, West Humber, Rexdale — all within 15 minutes of Pearson Airport

- Top-rated schools for families: The Kingsway, Edenbridge-Humber Valley, Princess-Rosethorn, Sunnylea

- Waterfront lifestyle: Mimico, Humber Bay Shores, Long Branch — higher pricing but waterfront parks, cycling trails, and lake access

- Best value new condo developments: Kipling Station area (from mid-$400,000s), The Queensway corridor (from mid-$400,000s), The East Mall (from $440,000)

For seniors who are sponsoring or being sponsored by family members and relocating to Etobicoke, ground-level homes in north Etobicoke neighbourhoods provide accessibility advantages over the high-rise buildings that dominate the south.

| Neighbourhood | 1-Bed Rent Range | Avg Home Price | Best For |

|---|---|---|---|

| Rexdale-Kipling | $1,719 – $1,956 | ~$734,000 | Affordable rent, newcomer community |

| Mount Olive-Silverstone | ~$2,009 | ~$620,000 – $706,000 | Lowest purchase entry point in Toronto |

| Smithfield / West Humber | $1,800 – $2,100 | $600,000 – $900,000 | Airport workers, students, budget families |

| Islington-City Centre | $2,000 – $2,600 | ~$900,000 – $1,130,000 | Subway access, mid-range pricing |

| Mimico / Humber Bay Shores | $2,000 – $2,850 | ~$778,000 – $915,000 | Waterfront, GO Transit, lifestyle |

| The Kingsway / Edenbridge | Limited rental stock | $1,130,000 – $2,300,000 | Premium schools, family homes |

Building Credit in Canada: The Foundation Every Newcomer Housing Decision Rests On

Your Canadian credit history is the single most important factor — after income — in determining your access to housing. A strong credit profile unlocks better mortgage rates, stronger rental applications, and more favourable terms on every financial product you use. Building it should start on day one.

The Credit-Building Timeline for Newcomers

- Month one: Open a Canadian bank account and apply for a secured or newcomer credit card. Use it for small purchases and pay the full balance every month without exception.

- Months one through six: Set up pre-authorized payments for your phone plan, internet, and any utility bills in your name. Consistent, on-time payments build your credit file.

- Months three through twelve: Apply for a small personal line of credit through your bank. Keep utilization low — ideally below 30 percent of your available limit.

- Month twelve and beyond: Check your credit score through one of Canada’s credit bureaus (Equifax or TransUnion). A score of 660 or higher positions you well for mortgage applications. A score above 700 opens the door to the most competitive rates.

Many Canadian lenders will also accept an international credit report as supporting documentation when Canadian credit is limited. If you have a strong credit history in your home country, ask your lender specifically about international credit documentation.

The connection between credit and housing is direct: a newcomer with a 700+ credit score and 5 percent down payment will qualify for a mortgage on a property up to $1.5 million with insured financing. A newcomer with no credit score may need 35 percent down — a dramatically different financial requirement. Every month you spend building credit before applying for a mortgage translates into real savings on your housing costs. Settling into affordable rental housing first while building credit is the strategy that positions most newcomers for successful homeownership within two to five years.

The Newcomer Housing Timeline: From Arrival to Ownership

The journey from landing in Canada to owning a home in Etobicoke is a sequence of deliberate, buildable steps. Rushing the process leads to overpaying, qualifying for worse mortgage terms, or choosing the wrong neighbourhood. Here is a realistic timeline based on how the most financially successful newcomers approach the process:

Phase One: First Three Months (Stabilize)

- Secure short-term or temporary rental housing — a furnished room, basement apartment, or corporate suite

- Open a Canadian bank account and credit card on day one

- Apply for your Social Insurance Number (SIN), OHIP health card, and Ontario photo card

- Register with a settlement agency for housing support and orientation

- Begin employment and establish income documentation

- If you have belongings arriving from overseas, coordinate freight delivery with your temporary housing address or a storage facility

Phase Two: Months Three through Twelve (Build)

- Transition from short-term to a one-year lease in a neighbourhood you have had time to evaluate

- Open an FHSA and begin contributing $8,000 per year toward your future down payment

- Build credit aggressively through on-time payments and responsible credit utilization

- Research Etobicoke neighbourhoods in person — visit on weekdays and weekends, at different times of day

- Connect with other newcomers in your neighbourhood through settlement agency community programs

Phase Three: Year One through Three (Prepare)

- Continue FHSA contributions ($24,000 over three years if maximized)

- Begin RRSP contributions if not already using them, with the Home Buyers’ Plan in mind ($60,000 maximum withdrawal)

- Get mortgage pre-approval to understand your exact budget — this does not commit you to purchasing

- Identify two to three target neighbourhoods based on your work location, school preferences, and lifestyle priorities

- Attend open houses to calibrate your expectations and understanding of different property types

Phase Four: Year Two through Five (Purchase)

- Execute your home purchase with FHSA + HBP funds, land transfer tax rebates, and HBTC credit

- Hire a real estate lawyer to manage the closing process (this is legally required in Ontario)

- Book your moving team at least two to four weeks before your closing date — moving dates near month-end and during summer are the busiest

- Coordinate utility transfers, address changes, and school registration if you have children

If you are downsizing from a larger rental into a purchased condo, or moving from a basement apartment into your first home, the logistics of each transition are different. High-rise condo moves require elevator booking and building insurance certificates. Detached house moves require careful furniture handling through doorways and stairwells. Professional packing protects your belongings — especially fragile items, electronics, and anything that survived an international journey to get here.

What a Newcomer’s Move to Etobicoke Actually Looks Like

Moving as a newcomer involves logistical layers that non-newcomers rarely face. Your belongings may be split between what you brought from your home country, what you purchased in temporary housing, and what you are inheriting or buying for your new permanent home. Coordinating all of it requires planning.

Metropolitan Movers Etobicoke has spent over 15 years serving Etobicoke’s diverse newcomer population. We understand the unique challenges of newcomer moves — from navigating language barriers during the coordination process, to handling possessions that have sentimental value spanning two countries, to working within tight budgets during the most expensive year of a newcomer’s Canadian journey.

Our services align with every stage of the newcomer timeline:

- Local moves between Etobicoke apartments — hourly and flat-rate options for moves within the same neighbourhood or across the city

- Long-distance relocations from other provinces — dedicated trucks with scheduled delivery windows for interprovincial transitions

- Full-service packing — professional handling of fragile, oversized, and high-value items using industry-grade materials

- Furniture transport — safe handling of heavy bedroom sets, dining tables, and oversized sofas through tight corridors and stairwells

- Piano and specialty item moving — for instruments that survived an international journey and need to be handled with equal care locally

- Temporary storage — secure facilities for belongings that arrive before your permanent home is ready

- Moves within the broader Toronto area — for newcomers who start in one part of the city and relocate to Etobicoke after finding their footing

- Office equipment relocation — for newcomer entrepreneurs or remote workers who need home office setups moved with care

Every quote is customized to your specific unit type, access conditions, building requirements, and volume of belongings. We provide honest numbers before moving day — not after.

The Decision That Shapes Everything Else: Why Getting Etobicoke Real Estate Right Matters for Newcomers

The housing decisions you make in your first years in Canada will compound over every year that follows. Choosing the right neighbourhood determines your commute time, your children’s school options, your grocery costs, your social network, and your long-term equity position. Choosing the right housing type — rental, condo, or freehold — determines your monthly cash flow and your exposure to the real estate market’s ups and downs. And choosing the right timing — rushing to buy before you are financially ready versus taking the disciplined path of building credit, saving strategically, and understanding the market — determines whether homeownership becomes a source of stability or stress.

Etobicoke real estate for newcomers in 2026 offers genuine opportunity. Prices have moderated from pandemic peaks. Interest rates have dropped from their recent highs. First-time buyer programs provide meaningful financial support. And Etobicoke’s neighbourhood diversity means there is a strong match for virtually every budget level, work location, and lifestyle preference — from the most affordable basement apartments in Rexdale to premium new condos along The Queensway to family homes in The Kingsway’s tree-lined streets.

Take the time to learn the market. Use the government programs available to you. Build your credit deliberately. Connect with settlement services early. And when you are ready to make the move — whether it is your first apartment or your first purchased home — Metropolitan Movers Etobicoke will be here with over 15 years of experience, transparent pricing, and the neighbourhood-level expertise that comes from serving every corner of this diverse, welcoming, and endlessly interesting part of Toronto.

Get your customized newcomer moving estimate today and take the next step toward making Etobicoke home.

Frequently Asked Questions About Etobicoke Real Estate for Newcomers

Can newcomers buy a home in Canada?

Yes. Permanent residents have the same property purchasing rights as Canadian citizens. Work permit holders can also purchase property, though mortgage terms may differ. The Prohibition on the Purchase of Residential Property by Non-Canadians Act restricts some foreign buyers, but permanent residents and most temporary residents with work permits are exempt from this restriction. Newcomers who have been in Canada within the past five years can access specialized newcomer mortgage programs offered through major Canadian banks and mortgage insurers.

What is the minimum down payment for newcomers buying in Etobicoke?

Permanent residents can purchase with as little as 5 percent down on homes priced up to $500,000, and 5 percent on the first $500,000 plus 10 percent on any amount above that for homes priced between $500,001 and $1.5 million. Newcomers without Canadian credit history may be required to provide a 35 percent down payment by some lenders in exchange for waiving the credit requirement. Mortgage insurance is mandatory for all purchases with less than 20 percent down.

What first-time buyer programs can newcomers use in Ontario?

Newcomers who are permanent residents can access the First Home Savings Account (up to $40,000 tax-free), the RRSP Home Buyers’ Plan (up to $60,000 per person), the Ontario Land Transfer Tax Rebate (up to $4,000), the Toronto Municipal Land Transfer Tax Rebate (up to $4,475), the Home Buyers’ Tax Credit ($1,500 federal tax savings), and extended 30-year amortization on insured mortgages. Combining all available programs, a qualifying couple could access up to $200,000 in tax-advantaged savings plus $8,475 in closing cost rebates.

How long does it take a newcomer to qualify for a mortgage?

Most newcomer mortgage programs require a minimum of three months of full-time Canadian employment. Building a Canadian credit score of 660 or higher typically takes six to twelve months of consistent credit card use and on-time bill payments. Many newcomers are mortgage-ready within 12 to 18 months of arrival, though those who arrive with substantial savings and international credit documentation may qualify sooner.

What are the most affordable Etobicoke neighbourhoods for newcomers?

Rexdale-Kipling, Mount Olive-Silverstone-Jamestown, Smithfield, West Humber-Clairville, and Thistletown offer the lowest housing costs in Etobicoke for both renters and buyers. One-bedroom apartments in these areas range from approximately $1,719 to $2,009 per month, while basement apartments start as low as $1,100 with utilities included. Home purchase prices start below $400,000 for condos in Mount Olive.

Where can newcomers find settlement and housing help in Etobicoke?

COSTI Immigrant Services, Albion Neighbourhood Services (Etobicoke Housing Help Centre), Newcomer Women’s Services Toronto, and the YMCA Newcomer Information Centre all serve the Etobicoke area with free, multilingual settlement and housing support. These organizations help with lease agreements, subsidized housing applications, government documents, and community connections. The IRCC settlement services directory lists all federally funded organizations by postal code.

What is the leasing process like for newcomers in the GTA?

Ontario law requires landlords to use the province’s Standard Lease form. Tenants pay first and last month’s rent upfront — no other deposits are legal. Rental applications typically require proof of employment, income documentation, photo ID, and a credit check authorization. Newcomers without Canadian credit can often substitute bank statements or international credit documentation. The Ontario Human Rights Code protects newcomers from discrimination based on place of origin, citizenship, or ethnic background.

Are there new condo developments in Etobicoke suitable for newcomers?

Yes. More than 60 pre-construction and recently completed projects are available across Etobicoke. Entry-level pricing starts in the mid-$400,000s for developments near Kipling station and along The Queensway corridor. Pre-construction purchases offer structured deposit schedules that give newcomers time to build savings. The average pre-construction cost per square foot in Etobicoke ranges from $700 to $1,200.

What is the Etobicoke market forecast for the rest of 2026?

Major real estate organizations forecast a measured recovery in sales volume and largely flat to modestly rising prices through 2026. There is substantial pent-up demand with over 100,000 buyers waiting on the sidelines in the GTA. Once economic conditions stabilize, analysts expect significant momentum in the second half of 2026 and into 2027. The current environment offers patient newcomer buyers favourable conditions — lower competition, longer days on market, and properties selling below asking price.

Should newcomers rent or buy in Etobicoke?

This depends entirely on your financial timeline. Newcomers who have been in Canada for less than a year should generally rent first — to build credit, establish employment, learn the city, and save a down payment. Newcomers who have been in Canada for two to five years, have built Canadian credit, saved through an FHSA and RRSP, and identified a target neighbourhood are well-positioned to buy. Rushing to purchase before your financial foundation is solid can lead to higher interest rates, weaker mortgage terms, and less negotiating power.

What settlement services will change in 2026?

Starting April 1, 2026, economic class permanent residents will only be able to access federally funded newcomer settlement services for a limited time. This makes it essential for newcomers to register with settlement agencies as early as possible after arrival — ideally within the first month. Registering early ensures access to housing help, language training, employment services, and community connections during the critical initial settlement period.